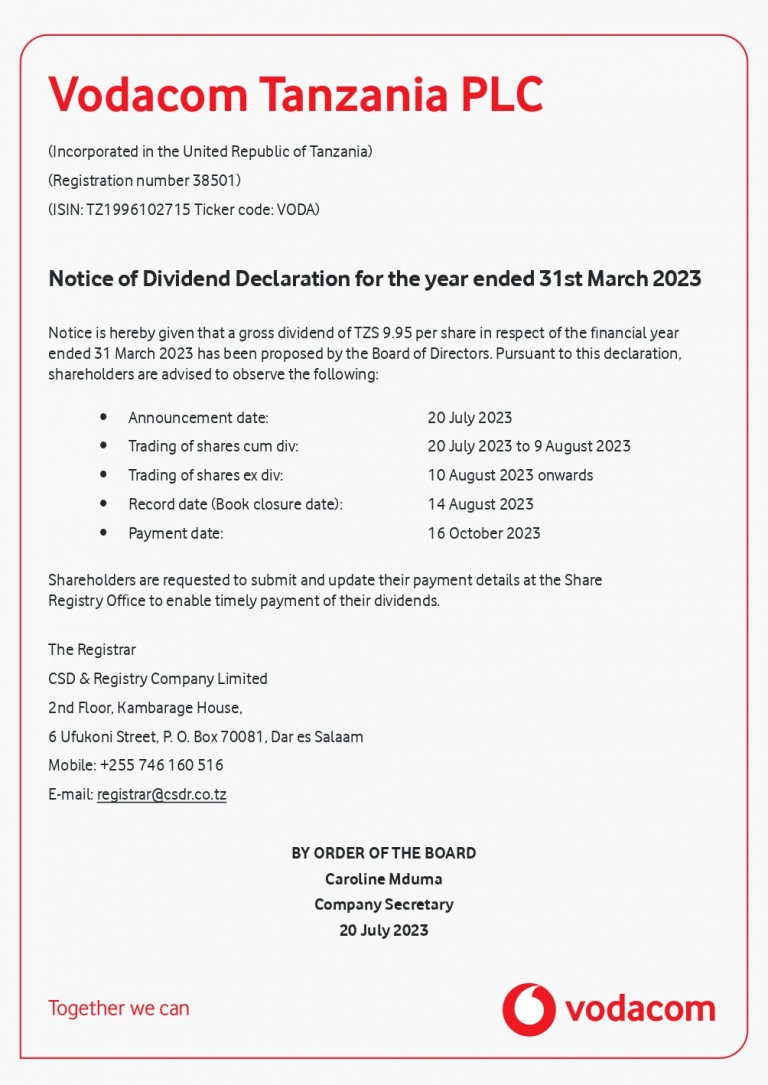

VODA – Dividend Declaration

THE Tanzania Portland Cement Plc (Twiga) has posted a pre-tax increase of 10.2 per cent in this year’s first half, thanks to production cost control measures. The oldest cement manufacturer in the country’s financial statement shows that the pre-tax profit…

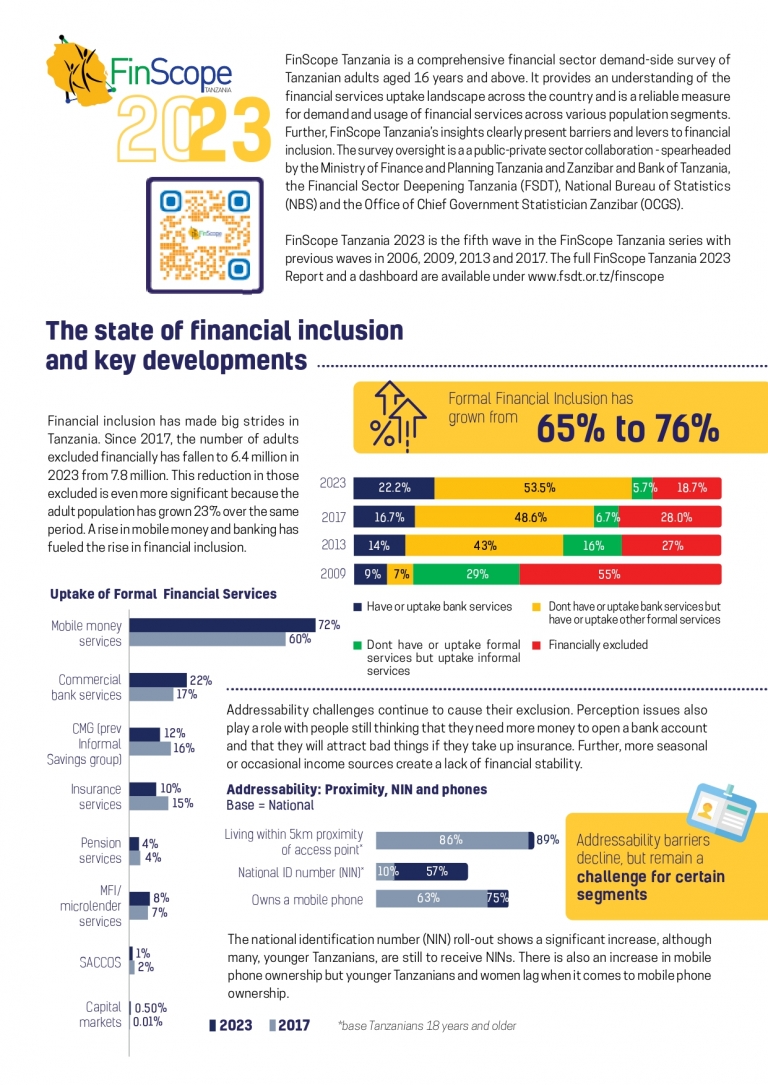

FinScope Tanzania is a comprehensive financial sector demand-side survey of Tanzanian adults aged 16 years and above. It provides an understanding of the financial services uptake landscape across the country and is a reliable measure for demand and usage of…

By The Citizen Reporter Dar es Salaam. The Bank of Tanzania (BoT) has permitted an African digital payments provider, DPO Pay, to operate as a Payment Service Provider in Tanzania, the company said in a statement yesterday. The DPO is registered…

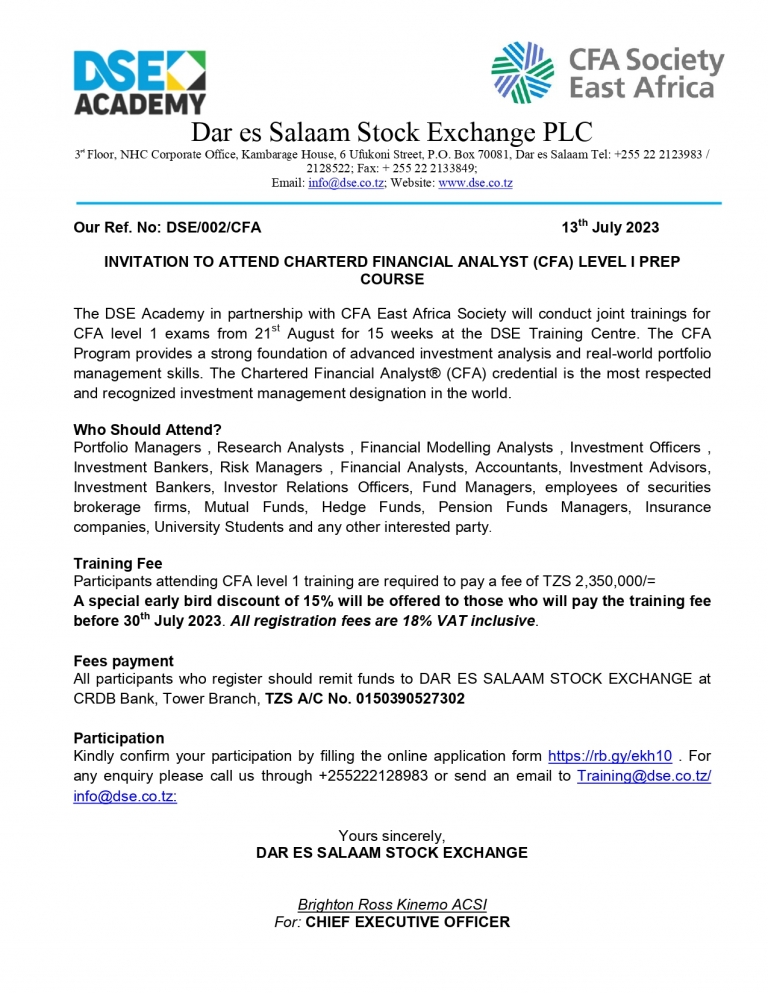

By Daily News Reporter THE turnover of the Dar es Salaam Stock Exchange (DSE) is projected to increase in the coming weeks as companies start to release their quarter two financials. The investors are banking on the firms’ good performance…

Is it a worthwhile investment to put money into the Dar es Salaam Stock Exchange? Judging from the performance of different stocks on the exchange and the performance of unit trusts that include equity stocks, one can confidently answer, YES,…

Dar es Salaam. Turnover at the Dar es Salaam Stock Exchange (DSE) fell by 30 percent during the 47th Dar es Salaam International Trade Fair (DITF) week. The fall was largely fuelled by the prolonged trend of low foreign investor…

Dar es Salaam. Global economic uncertainties, including trade tensions and geopolitical risks, contributed to more cautious investor sentiment towards frontier markets such as Tanzania in the first half of 2023. As a result, trading at the local equities market declined, with…